Introduction

From Racine to Rhinelander, everyone in Wisconsin deserves the freedom to make a good living and care for our families. However, the tax plan proposed by Republican legislative leadership would further rig the rules in favor of the wealthiest and make Wisconsin’s glaring racial disparities even worse. The four proposals leave everyday families even further behind because none of these tax proposals effectively target families who are struggling to make ends meet. Giving most of the nearly $2 billion per year to the wealthy makes it harder to invest in the critical resources low and middle-income families need: infrastructure, child care, health care, and schools.

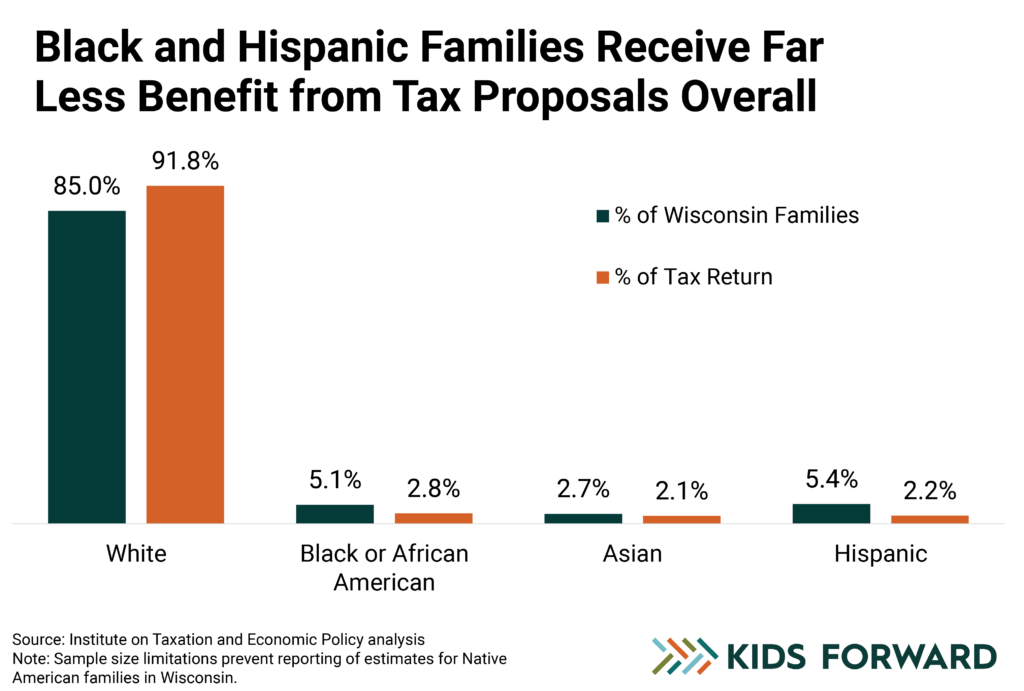

The tax plan proposed by Republican leadership disproportionately hurts families of color.

An analysis by the Institute on Taxation and Economic Policy (ITEP) shows that these tax cuts will disproportionately benefit white households. Discriminatory housing policies and predatory lending practices have denied access to homeownership and generational wealth to families of color for decades. This has left families of color overrepresented in the lowest income bracket (making $32,400 or less). As a result, families of color overall would see virtually no benefit from the tax cuts.

Furthermore, Wisconsin’s economic foundation relies on the hard work of immigrants. Undocumented immigrants work and contribute to Wisconsin’s prosperity, paying $101.1 million in state and local taxes in 2018. Yet, these parents and caregivers are not eligible for the public benefits their investments produce.

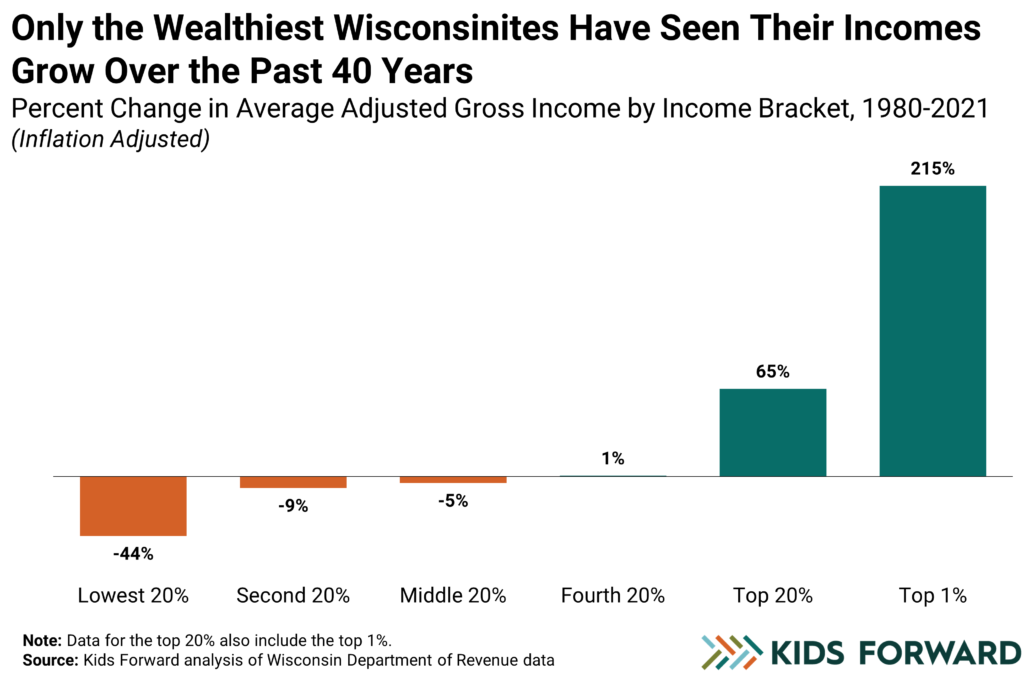

More than half of proposed tax cuts go to the wealthiest Wisconsinites.

An analysis by the ITEP shows that 59% of the proposed tax cuts would line the pockets of Wisconsin’s wealthiest – households that make an average of $308,800 per year and are overwhelmingly white. In the last four decades, Wisconsin’s wealthiest residents have seen explosive growth in their incomes, while everyone else has seen no increase or watched their income decline. These tax cuts will only make the problem worse.

Wisconsinites move for jobs, family, housing, and weather. Not taxes.

Among the most important reasons people decide to move, the most common are job opportunities, proximity to family, the cost of housing, and weather. One thing that doesn’t make the cut: taxes. An analysis of available evidence shows that a large majority of movers reported they were moving for jobs or family.

Tax cuts for Wisconsin’s wealthiest could undermine efforts to build affordable housing, strong public education systems, infrastructure, and other public services that make Wisconsin attractive to workers and families. Tax cuts for Wisconsin’s wealthiest could cause serious harm, especially at a time when state budgets are under increasing strain due to factors such as expiring federal relief funds and a modestly cooled economy.

About the Proposals

Personal income tax (AB 1020)

Expanding the 4.4% tax bracket is a tax cut that will disproportionately benefit Wisconsin’s wealthiest families, who are overwhelmingly white, and would cost us nearly $800 million. Households in the top 20% of income earners, with an average income of $308,800, would see over 56% of those tax savings.

This tax cut would also make Wisconsin’s tax system more regressive. According to the ITEP’s most recent edition of Who Pays?, Wisconsin’s low- and middle-income families already pay more of their income in state and local taxes than the state’s wealthiest residents. This would make it worse.

Retirement exemption (AB 1021)

Tax systems work best when they focus on ability to pay, not age. Allowing all retired Wisconsinites to exempt up to $150,000 of their income will not even center the seniors that actually need it most. Retirees making upwards of $1 million per year would get to claim the exemption. This exemption would cost Wisconsin over $466 million annually, and 58% of this tax cut would go to households in the top 20% with average incomes of $308,800.

Child and dependent care tax credit (AB 1023)

Affordable childcare is an increasingly important issue for Wisconsin’s working families, but this proposal does not solve the problem for many reasons. The proposed credit is nonrefundable, meaning the policy excludes low-wage working families, who struggle the most to afford sustainable childcare. An ITEP analysis of which households would benefit the most from the credit shows that households in the top 20% by income would receive 56%of the benefit of the credit expansion. The lowest-paid Wisconsinites, who struggle the most to afford childcare, would benefit very little.

Marriage credit (AB 1022)

As part of the overall tax package, this proposal’s non-refundability contributes to the package’s overall regressivity.

***

By Emily Miota & William Parke-Sutherland